The Enterprise AI Illusion: Token Economics, Open-Source Models, and the UK Data Sovereignty Crisis in 2026

Quick Summary

By mid-2026, 97% of UK businesses report critical AI skills gaps whilst frontier model costs have reached $10 per million input tokens for Claude Fable 5, trapping enterprises in a cycle of proprietary dependency that prevents migration to open-weight models like GLM-5.2, which scores 62.1% on SWE-bench Pro — outperforming GPT-5.5's 58.6% — under an unrestricted MIT licence.

Specialist UK AI agencies including Faculty AI, Viston AI, and Classic Informatics are bridging the last mile by constructing model-agnostic routing systems that divert routine workloads to quantised open-source models at $4.74 per million tokens — an 84% cost reduction versus AWS cloud pricing of $29.09 — whilst reserving frontier API calls for complex edge-case reasoning tasks.

A 12 June 2026 US Commerce Department directive that instantly disabled Anthropic's Fable 5 and Mythos 5 for all non-US users has exposed the kill-switch vulnerability of foreign AI dependency, making UK GDPR-compliant, version-pinned open-weight deployments on sovereign infrastructure such as OnshoreAI's AWS London (eu-west-2) environment the only architecturally sound foundation for UK regulated enterprise AI.

Table of Contents

An extraordinary 97% of UK businesses report at least one critical AI skills gap in 2026 — yet the frontier models draining their IT budgets are no longer the best tools for the job.

UK enterprises find themselves ensnared in a costly paradox. Highly capable open-weight AI models now match or outperform expensive proprietary platforms like Anthropic's Claude and OpenAI's GPT on routine workloads — yet the vast majority of British businesses cannot make the switch. The technical complexity required to deploy open-source models safely lies far beyond the capacity of overburdened IT departments, forcing organisations to continue paying premium per-token rates to US-hosted providers. Meanwhile, a June 2026 export-control directive proved, devastatingly, that those providers can revoke access to critical enterprise infrastructure without warning.

This analysis examines the structural frictions holding UK enterprises back from sovereign, cost-efficient AI architecture — and the strategic path to breaking free.

Table of Contents

- The Last Mile Problem: Why Open-Source Feels Unreachable - The UK AI Talent Crisis: A Structural Breakdown - The True Cost of Token Maxing - Data Sovereignty vs. Data Residency: A Dangerous Confusion - The Open-Source Performance Breakthrough: GLM-5.2 and Outcome Maxing - The UK Agency Opportunity: Bridging the Last Mile - Key Takeaways - Conclusion

The Last Mile Problem: Why Open-Source Feels Unreachable

Power up with ClickUp

"Is your team drowning in tabs? ClickUp saves 1 day a week per person. That's a lot of Fridays."

For most UK businesses, adopting a frontier AI model like OpenAI's GPT-5.6 or Anthropic's Claude Fable 5 requires nothing more than a credit card and an API key. This frictionlessness is the proprietary model's single greatest competitive advantage — and its most dangerous trap. It creates artificial switching costs that have nothing to do with model capability and everything to do with deployment complexity.

Deploying an open-weight model like Zhipu AI's GLM-5.2 requires an organisation to construct an entirely bespoke cognitive architecture from scratch. Operating this 744-billion-parameter model — which uses a Mixture-of-Experts (MoE) design activating only roughly 40 billion parameters per token — demands sophisticated engineering across every layer of the deployment stack. Teams must build memory architectures, dynamic prompt construction pipelines, context window management systems, Retrieval-Augmented Generation (RAG) integrations, and autonomous tool-calling harnesses.

Quantisation management alone represents a non-trivial engineering discipline. Applying Unsloth's dynamic 1-bit or 2-bit quantisation formats, for instance, compresses GLM-5.2 from its raw footprint to 239GB of disk space whilst retaining approximately 82% of its raw accuracy — making frontier-class open-weight models viable on accessible enterprise hardware rather than requiring bespoke GPU clusters. Architectural breakthroughs like IndexShare, which reuses indexers across sparse attention layers to reduce per-token compute by nearly three times, deliver dramatic efficiency gains — but only to organisations with dedicated Machine Learning Operations (MLOps) engineers capable of implementing and maintaining them.

The Harness Engineering Challenge

The engineering challenge runs deeper than compute provisioning. Each enterprise workflow must be decomposed into discrete, task-specific harnesses capable of managing model hallucinations, orchestrating sub-agent calls, and maintaining state across extended multi-step operations. Breaking complex organisational processes into parallel harness architectures allows teams to scale output whilst controlling error rates — but these pipelines are architecturally sophisticated systems that bear no resemblance to the configuration work familiar to standard IT functions.

For the vast majority of UK IT departments, these are not peripheral concerns requiring upskilling. They are entirely foreign disciplines that demand purpose-built specialist engineering teams. Traditional IT support functions, focused on licence management, infrastructure maintenance, and helpdesk operations, lack even the conceptual vocabulary to evaluate open-weight model deployments, let alone design and operate them at production scale.

The result is a structural impasse: organisations intellectually aware of the economic arguments for open-source AI, but entirely unable to traverse the final and most technically demanding stretch of the deployment journey. This mirrors the broader challenge explored in our guide to multi-agent AI frameworks like LangGraph and CrewAI, which similarly demand engineering resources that most UK enterprises cannot source internally.

The UK AI Talent Crisis: A Structural Breakdown

The last mile problem is not simply a matter of organisational ambition or risk tolerance. It is a direct consequence of a deeply dysfunctional UK AI labour market that has failed to produce the specialised engineering talent enterprises require.

By mid-2026, the talent shortfall has reached acute levels across every technical dimension of AI deployment. The Department for Science, Innovation and Technology (DSIT) 2025 AI Labour Market Survey reveals that 57% of UK businesses face severe technical AI skills deficiencies, specifically in advanced modelling, machine learning, and systems architecture. Most alarmingly, the gap in foundational AI knowledge has actually widened — from 55% of organisations reporting deficiencies in 2020 to 60% in 2025/26, despite five consecutive years of accelerating market adoption. Adoption has outrun capability at every level.

The Salary Arms Race

The scarcity of qualified AI engineering personnel has driven salary inflation to levels prohibitive for all but the largest technology-native firms. The UK market for AI talent now operates as a fierce bidding war in which standard enterprises simply cannot compete with hyperscalers and specialist consultancies.

| AI Engineering Role (UK 2026) | Salary Range | Key Market Dynamic |

|---|---|---|

| Prompt / Integration Engineer | £90,000 – £120,000 | Entry-level positions commanding extreme premiums due to sudden demand spikes |

| Machine Learning Engineer | £70,000 – £130,000 | Compensation heavily dependent on MLOps and deployment expertise |

| AI Director / Head of AI | £200,000+ | Highly concentrated in London and South East; commands a 23% wage premium over non-AI leadership roles |

This concentration is geographically acute. Sixty per cent of all expert-level AI vacancies are clustered in London and the South East, creating a virtual talent desert for regional businesses across the Midlands, the North, and Wales. A professional services firm in Leeds or a manufacturing business in Cardiff faces a hiring environment in which the available pool of open-source AI deployment engineers is vanishingly small — and where any candidate accepting a role can expect a competing offer within months.

A full 28% of UK organisations confirm that technical skills shortages have directly prevented them from achieving core business objectives, whilst an estimated 40% of potential AI productivity gains are being wasted because workforces cannot properly deploy or integrate the technology they already license.

The Training Paradox

Faced with unaffordable external recruitment, organisations attempt to develop talent internally. Yet research reveals a deeply counterproductive dynamic. Employees who receive more than 81 hours of structured annual AI training — those genuinely capable of building open-source deployment pipelines — experience productivity gains of up to 14 hours per week. These same employees, however, become dramatically more marketable. They are 59% more likely to leave their current employer within 18 months. This dual reality deters 62% of UK employers from committing to comprehensive AI upskilling programmes.

The TESS Group AI Adoption Index confirms the systemic consequence: most UK organisations remain stuck at the "Experimenting" or "Adopting" phase of AI maturity, where staff self-teach via informal shadow IT usage. They consistently fail to reach the "Embedding" level where trained teams design and operate real, production-grade AI workflows.

There is a structural shift toward apprenticeship routes — AI hires through apprenticeships rose from 3% in 2020 to 19% in 2025, heavily supported by the 2026 Growth and Skills Levy — but this pipeline is too slow to solve immediate operational needs. Faced with the practical reality of paying over £100,000 for a machine learning engineer who may depart within 18 months, most UK IT departments capitulate. They default to enterprise contracts with Anthropic, Google, or OpenAI, trading a steep but bounded capital expenditure for a spiralling, unpredictable operational expenditure in per-token API charges.

The True Cost of Token Maxing

The era of subsidised, flat-rate AI pricing is definitively over. By 2026, 85% of SaaS providers have transitioned to consumption-based pricing models tied directly to token usage, exposing the true financial weight of embedding frontier models into enterprise operations. For UK organisations that have scaled AI usage without implementing cost controls, the consequences are severe.

The Geometric Explosion of Agentic Costs

The fundamental misunderstanding in most UK enterprise AI budgets is the dramatic difference between conversational AI usage and agentic AI usage. A human employee interacting with an AI assistant for email summarisation might consume 10,000 tokens daily — a manageable and predictable expenditure at almost any model tier. An autonomous agentic system executing multi-step coding migrations, document processing pipelines, or customer data analysis workflows can consume tens of millions of tokens in the same timeframe.

Agentic costs scale geometrically: agents trigger sub-agents, execute recursive tool calls, parse massive document corpora, and maintain extended conversational state, compounding charges at every algorithmic decision point. The pricing variance between available models represents a 4,500x spread between budget production models and the most expensive frontier reasoning engines — a differential that maps directly onto operational expenditure when workloads are misrouted.

| Frontier Model (June 2026) | Input Cost (per 1M tokens) | Output Cost (per 1M tokens) | Context Window |

|---|---|---|---|

| Claude Fable 5 | $10.00 | $50.00 | 1,000,000 tokens |

| Claude Opus 4.8 | $5.00 | $25.00 | 200,000 tokens |

| GPT-5.6 Sol Tier | $5.00 | $30.00 | 128,000 tokens |

| Gemini 3.1 Pro | $2.00 | $12.00 | 2,000,000 tokens |

| Claude Sonnet 4.6 | ~$3.00 | ~$15.00 | 200,000 tokens |

The financial consequences of undifferentiated frontier model usage are catastrophic at scale. In a widely publicised incident, Uber granted 5,000 engineers access to Claude Code in December 2025; by April 2026, the company had exhausted its entire annual AI budget. This is not an anomaly — it is the predictable result of deploying agentic systems at enterprise scale without intelligent cost routing.

Token Maxing vs. Outcome Maxing

UK IT managers currently engage in what analysts call "token maxing" — defaulting to the most expensive frontier models for every query, driven primarily by employee brand recognition rather than task requirements. The economic irrationality of this behaviour is easily demonstrated: a basic 500-line code review processed through Claude Fable 5 costs $0.18, whilst the identical task routed to the more appropriate Sonnet 4.6 costs $0.05. Scaling this differential across a multi-day autonomous coding migration pushes Fable 5 costs past $100 per execution whilst Sonnet delivers the same functional output for a fraction of the spend.

The overwhelming majority of routine enterprise workloads — extracting text from invoices, summarising internal meetings, classifying support tickets, generating boilerplate documentation — require no frontier reasoning capability whatsoever. These tasks sit firmly in the "centre of distribution": familiar, highly repetitive, and entirely achievable by smaller, optimised open-source models at a fraction of the cost.

The strategic discipline of "outcome maxing" demands that organisations rigorously categorise their workloads and match each category to the cheapest model capable of delivering the required outcome. Implementing this discipline requires the same engineering capability needed for open-source deployment — which returns us directly to the talent problem. For finance teams modelling the business case for this transition, the CFO's guide to AI ROI for UK finance directors provides a detailed quantification framework.

Data Sovereignty vs. Data Residency: A Dangerous Confusion

Beyond token cost economics lies an equally pressing strategic crisis: the systematic conflation of "data residency" with "data sovereignty" among UK IT leadership, a confusion that creates compliance vulnerabilities whilst providing organisations with a false sense of security.

The Residency Illusion

Major US AI providers routinely market "EU data residency" options — physically storing data on servers in Frankfurt or Paris — as a compliance solution for European and British enterprises. This is a legally meaningless proposition for UK organisations on two distinct grounds. Following Brexit, the United Kingdom operates as an entirely separate data-protection jurisdiction from the European Union. Routing UK enterprise data to Frankfurt servers technically constitutes an international cross-border transfer, not a domestic data handling arrangement.

More critically, data residency specifies only where a hard drive is physically located. It says nothing whatsoever about legal jurisdiction over that data. If a US-headquartered company operates those servers, the data remains fully subject to extraterritorial US legislation — most notably the CLOUD Act and FISA Section 702. Both statutes compel American companies to hand over data upon government request, regardless of the physical location of the servers. No data processing agreement or contractual clause between a UK enterprise and a US AI provider can override these statutory compulsions.

True data sovereignty requires exclusive legal and technical jurisdiction: ensuring that the software processing the data operates entirely outside the reach of third-country legal claims and cannot be compelled by foreign government directives. For UK businesses handling sensitive commercial data, proprietary intellectual property, personal data regulated under UK GDPR, or data subject to sector-specific regulatory requirements, this distinction is not academic — it is a legal and operational imperative. The UK Data Act 2025 survival guide and the FCA AI compliance guide for UK fintech provide essential context for regulated sector obligations.

Shadow AI and the Compliance Unravelling

The data sovereignty problem is dramatically compounded by the explosion of unsanctioned AI usage across UK enterprises. The phenomenon of "Shadow AI" — employees utilising unauthorised generative AI tools to complete routine work outside IT oversight — has created a genuine compliance emergency. Organisations now observe an average of 66 different generative AI applications in simultaneous use across their workforces, of which 10% are classified as high risk.

Without IT governance, employees routinely paste sensitive commercial data, client confidential information, regulated personal data, and proprietary strategic documents into external AI systems, completely bypassing the data handling controls mandated by UK GDPR and corporate security policies. The consequence is a 2.5x increase in data loss prevention (DLP) incidents across the enterprise AI landscape. Each of these incidents represents a potential regulatory notification obligation, reputational liability, and in regulated sectors, a reportable breach.

The Kill Switch Materialises

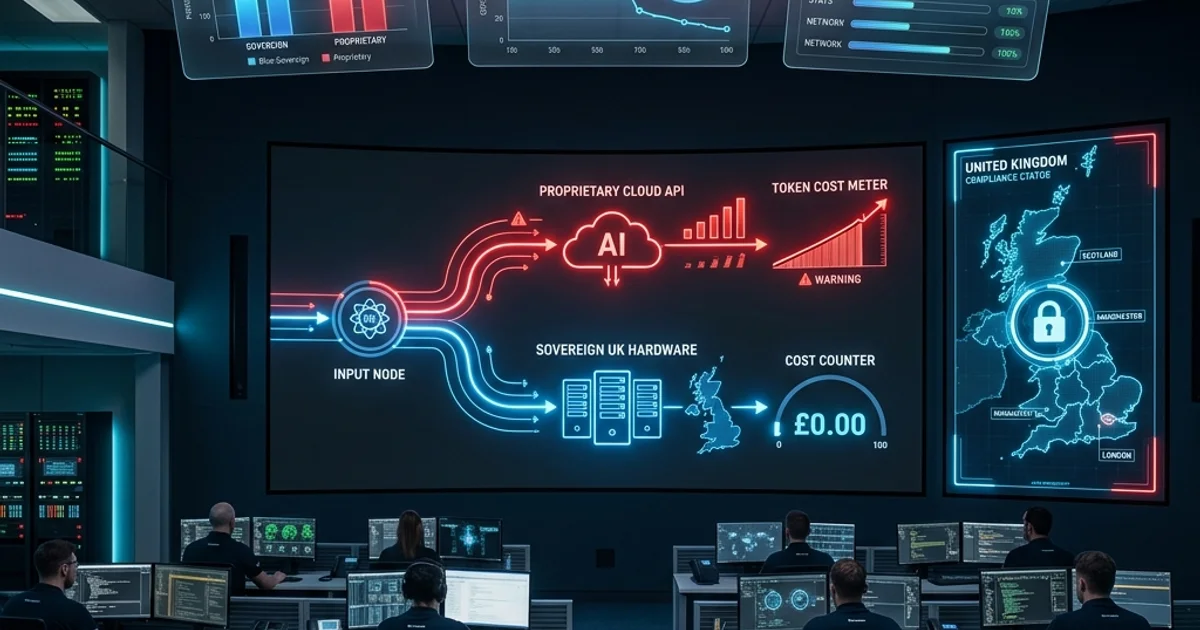

The theoretical risk of depending on proprietary, foreign-controlled AI systems became devastatingly concrete on 12 June 2026. A US Commerce Department export-control directive compelled Anthropic to immediately disable access to two of its most capable models — Fable 5 and Mythos 5 — for all non-US users. Within hours, UK enterprises deeply embedded in the Anthropic ecosystem lost access to critical operational infrastructure with no migration path and no operational alternative.

This event crystallised a structural vulnerability that informed observers had long documented: proprietary AI models carry an inherent kill switch, controlled not by the enterprise customer but by the vendor's domestic government. The suddenness of the June 12 disruption — immediate, without transition period — exposed the genuine operational fragility of proprietary dependency at exactly the moment UK organisations had scaled their reliance on these models into production-critical workflows.

Open-weight models hosted on UK-sovereign compute are, by architectural design, immune to this vulnerability. Providers such as OnshoreAI, operated by UK-based Hostcomm and running entirely within AWS London (eu-west-2) under ICO-registered processors, demonstrate a credible sovereign deployment model. By pinning exact model versions to specific release points, enterprises maintain stable compliance with Data Protection Impact Assessments (DPIAs) without the risk of upstream vendor changes silently altering model behaviour or availability. The strategic case for this approach is explored in depth at Sovereign AI and local LLMs for UK businesses.

The Open-Source Performance Breakthrough: GLM-5.2 and Outcome Maxing

The principal historical objection to open-source AI — inferior capability — no longer holds. The economic and strategic argument for defaulting to proprietary frontier models has effectively collapsed with the emergence of frontier-class open-weight models in mid-2026.

GLM-5.2: The Performance Case

Zhipu AI's GLM-5.2, released under an unrestricted MIT licence, is the most consequential demonstration of open-source capability parity to date. The model's MoE architecture delivers 744 billion total parameters whilst activating only approximately 40 billion per token, maintaining frontier-level performance at dramatically reduced compute overhead — enabling deployment on enterprise-grade hardware rather than bespoke GPU clusters.

On the benchmarks that matter for enterprise deployment, GLM-5.2 matches or exceeds the proprietary leaders:

| Benchmark | GLM-5.2 | GPT-5.5 | Claude Opus 4.8 |

|---|---|---|---|

| SWE-bench Pro (software engineering) | 62.1% | 58.6% | ~60% |

| Terminal-Bench 2.1 (agentic task execution) | 81.0% | ~77% | 85.0% |

| Artificial Analysis Intelligence Index | Premier open model ranking | Below | Marginally ahead |

| Context Window | 1,000,000 tokens | 128,000 tokens | 200,000 tokens |

| Licence | MIT (unrestricted commercial use) | Proprietary | Proprietary |

GLM-5.2 currently ranks as the premier open model on the Artificial Analysis Intelligence Index, significantly outperforming GPT-5.5 on software engineering tasks whilst offering a 1-million-token context window that neither proprietary competitor provides at any price point. For the centre-of-distribution workloads that constitute the overwhelming majority of UK enterprise AI usage, GLM-5.2 is not a compromise — it is a superior choice.

The Token Economics of Owned Infrastructure

Deploying GLM-5.2 or comparable open-weight models on-premise transforms the fundamental economic model of enterprise AI. The shift from variable operational expenditure — per-token metering with no ceiling — to a fixed asset model with owned compute introduces the discipline of Token Economics, where the primary performance metric becomes Tokens Per Second per Dollar (TPS/$) rather than raw capability benchmarks.

Hardware-native optimisation on enterprise servers delivers returns that dwarf cloud API economics. Operating a Lenovo configuration with NVIDIA B300 hardware on-premise reduces the cost per million tokens to $4.74 — an 84% cost reduction compared to renting the identical compute through AWS on-demand pricing at $29.09 per million tokens. This is not a marginal efficiency gain; it is a structural transformation of the unit economics of AI deployment.

The break-even point for migrating from a proprietary API to self-hosted open-source typically triggers between 3 and 5 million AI queries per month. Beyond this threshold, each additional query processed by an owned model drives marginal inference cost progressively toward zero, permanently decoupling the organisation's AI capability from the volatility of external token markets. For organisations operating agentic AI systems at scale, this break-even accelerates dramatically — agentic workloads that would cost tens of thousands monthly on Fable 5 become effectively free beyond the amortised hardware investment.

The UK Agency Opportunity: Bridging the Last Mile

The convergence of a domestic talent shortage, escalating token costs, catastrophic data sovereignty failures, and the sudden viability of frontier-class open-source models has created an extraordinary commercial opportunity for specialised UK technology consultancies equipped to build the harnesses that enterprises cannot construct internally.

Model-Agnostic Routing: The Architecture of Outcome Maxing

The most sophisticated UK AI agencies are positioning themselves not as systems integrators but as enterprise architects designing intelligent, model-agnostic routing middleware. This architecture intercepts every AI request within an enterprise environment and dynamically routes it to the cheapest model capable of delivering the required output quality.

Under this model, routine summarisation requests are automatically diverted to a self-hosted, quantised open-weight model at fractional cost per query. Complex legal reasoning tasks are escalated to a proprietary frontier API. Extended multi-step research operations requiring vast context are routed to GLM-5.2's 1-million-token window on sovereign infrastructure. To the end-user, the experience is seamless and identical across all query types; to the finance department, the token bill contracts by 10x to 50x — representing savings of up to 98% on high-volume automated pipelines — whilst output quality remains indistinguishable from full frontier model usage.

The Bifurcated UK Agency Market

The UK consulting landscape has rapidly stratified into three distinct tiers, each addressing a different segment of enterprise AI demand and operating on fundamentally different engagement models:

| Consultancy Tier | Target Client Segment | Representative Agencies | Primary Delivery Focus |

|---|---|---|---|

| Big 4 / Enterprise Consultancies | FTSE 250, Large Public Sector | PwC, Deloitte, IBM Consulting | AI transformation governance, compliance, global delivery frameworks |

| Specialist AI Boutiques | Mid-Market, Regulated Sectors | Faculty AI, Viston AI, Classic Informatics | Custom ML models, MLOps, intelligent routing, agentic workflow design |

| Agile Automation Agencies | UK SMEs, E-commerce, Professional Services | Elevate AI, Flowio, Automaly, MQLFlow | Rapid n8n workflows, CRM integration, voice AI, pilot-first automation |

Faculty AI occupies the premium end of the specialist boutique tier, building custom models and governance frameworks for environments — defence, NHS, central government — where data sovereignty and model interpretability are non-negotiable requirements rather than desirable features. Based in London, the heart of Europe's largest AI hub, Faculty draws on UCL and Imperial College graduate networks to provide engineering depth unavailable elsewhere in the UK market.

For organisations that cannot wait for recruitment pipelines, embedded engineering partners like Classic Informatics provide complete AI-augmented development teams on a fractional basis, bypassing the UK hiring market entirely. At the SME level, agencies such as Elevate AI and Flowio deploy pilot-first engagement models, enabling smaller UK businesses to automate specific workflows and validate measurable ROI before committing to broader transformation. This approach mirrors the strategic value of fractional AI leadership for UK SMEs, extending the fractional model from C-suite leadership to full engineering capability.

Regional Ecosystems: The Wales Case Study

The effort to bridge the AI capability gap is not confined to London's technology ecosystem. Regional initiatives are deploying substantial capital and specialised expertise to deliver the last mile of AI deployment to businesses that cannot access metropolitan consultancy talent or afford the salary premiums required to hire internally.

Wales provides the most comprehensive example of coordinated regional AI capability-building. The Welsh Government recently committed a £2.1 million support package specifically designed to help SMEs adopt AI ethically and effectively. This includes £600,000 for Business Wales awareness programmes and £1 million directed through the Flexible Skills Programme, where employers contribute only 25% of upskilling costs — making professional AI engineering training accessible at a fraction of typical market rates.

The Hartree Centre Cardiff Hub acts as a proxy engineering team for businesses that cannot afford dedicated ML engineers, providing free, targeted AI and data analytics support across the Cardiff Capital Region and the Western Gateway. Real-world deployments demonstrate practical impact across sectors:

- SimplyDo — working with sensitive sectors including defence and policing, required absolute data sovereignty. The Hartree Centre provided technical knowledge transfer enabling SimplyDo to deploy open-source models entirely in-house, ensuring all customer data was processed within UK jurisdiction without exposure to foreign AI providers. - GroupEd — an EdTech startup embedded large language models into its platform to process school data and provide translation services, freeing significant administrative resource for educational staff. - Rusty Design — received generative AI recommendations for automating digital asset creation, directly securing Innovate UK Creative Catalyst funding. - Something Different Wholesale — a Swansea-based £11 million turnover giftware business implemented AI for market insight, task automation, and global web page translation using Welsh Government support funding.

Simultaneously, Media Cymru — a £50 million strategic programme led by Cardiff University — is driving AI adoption in the creative sector, helping media organisations transition to generative AI workflows whilst protecting editorial voice and authorial identity. These regional cluster models demonstrate that sovereign, cost-efficient AI deployment is deliverable beyond the M25 through localised, embedded expertise — and they provide a replicable template for how UK regions can build genuine AI capability rather than perpetuating dependency on foreign proprietary providers.

Looking for the Best AI Agents for Your Business?

Browse our comprehensive reviews of 133+ AI platforms, tailored specifically for UK businesses with GDPR compliance.

Explore AI Agent ReviewsNeed Expert AI Consulting?

Our team at Hello Leads specialises in AI implementation for UK businesses. Let us help you choose and deploy the right AI agents.

The enterprise AI illusion is breaking down across the UK corporate landscape. The comfortable assumption that signing an enterprise contract with Anthropic, Google, or OpenAI represents a complete, compliant, and economically sustainable AI strategy has been exposed as fundamentally flawed on three simultaneous fronts: cost, sovereignty, and resilience.

The token cost crisis is real and accelerating. Organisations that have embedded frontier models into agentic workflows without implementing intelligent routing are haemorrhaging IT budgets at a rate that compounds with every additional automated process they deploy. The discipline of outcome maxing — matching workloads to the cheapest model capable of delivering the required output — is no longer a competitive optimisation. It is the defining operational competence of any enterprise that expects to sustain its AI investment beyond the next budget cycle.

The data sovereignty illusion must be replaced by genuine architectural sovereignty. The June 12 kill-switch event removed any remaining ambiguity: UK businesses handling sensitive, regulated, or commercially critical data cannot rely on US-controlled proprietary models as primary AI architecture. Open-weight models hosted on UK-sovereign compute, properly governed and version-pinned for DPIA compliance, represent the only architectural foundation that is immune to foreign government directives, vendor pricing changes, and sudden capability withdrawals.

The talent crisis is structural and will not resolve through recruitment alone. The 97% skills gap will not close by waiting for the labour market to catch up. UK enterprises must choose between two viable strategies: intensive, structured internal upskilling programmes supported by Growth and Skills Levy funding, or immediate engagement with the growing ecosystem of specialised UK AI agencies capable of building the harnesses, routing systems, and sovereign deployment pipelines that internal teams cannot construct.

For the overwhelming majority of UK organisations, the most financially prudent path is to engage specialist partners who have already traversed the last mile — and to do so before the next kill switch is thrown.

Key Takeaways

- 97% of UK businesses report at least one critical AI skills gap in 2026, with 57% facing severe technical deficiencies specifically in advanced modelling, machine learning, and systems architecture.

- The UK AI talent shortage is structurally worsening: the gap in foundational AI knowledge widened from 55% of organisations in 2020 to 60% in 2025/26 despite five consecutive years of accelerating adoption.

- AI Director salaries exceed £200,000 in the UK market, commanding a 23% wage premium over equivalent non-AI leadership roles, with 60% of expert-level vacancies concentrated in London and the South East.

- 85% of SaaS AI providers shifted to consumption-based token pricing by 2026, exposing a 4,500x pricing spread between budget production models and premium frontier reasoning engines.

- Claude Fable 5 costs $10 per million input tokens and $50 per million output tokens — double its predecessor — making unmanaged enterprise agentic deployments financially catastrophic at scale.

- On-premise deployment of GLM-5.2 on NVIDIA B300 hardware reduces per-million-token costs to $4.74, an 84% cost reduction versus equivalent AWS on-demand cloud pricing of $29.09 per million tokens.

- GLM-5.2 scored 62.1% on SWE-bench Pro, outperforming GPT-5.5's 58.6%, whilst offering a 1-million-token context window under an unrestricted MIT licence enabling full commercial self-hosting.

- On 12 June 2026, a US Commerce Department directive forced Anthropic to immediately disable access to Fable 5 and Mythos 5 for all non-US users, demonstrating the operational kill-switch risk of foreign proprietary AI dependency.

- Shadow AI has produced an average of 66 generative AI applications in simultaneous use across UK enterprises, with 10% classified as high risk and driving a 2.5x increase in data loss prevention incidents.

- The Welsh Government committed £2.1 million to SME AI adoption support, including £1 million through the Flexible Skills Programme where employers pay only 25% of upskilling costs under the 2026 Growth and Skills Levy.

TTAI.uk Team

AI Research & Analysis Experts

Our team of AI specialists rigorously tests and evaluates AI agent platforms to provide UK businesses with unbiased, practical guidance for digital transformation and automation.

Stay Updated on AI Trends

Join 10,000+ UK business leaders receiving weekly insights on AI agents, automation, and digital transformation.

Related Articles

Sovereign AI and Local LLMs: The Future of UK Business

Directly covers deploying open-weight models on UK-sovereign infrastructure to eliminate the foreign vendor kill-switch risk analysed in this article.

CFO Guide to AI ROI for UK Finance Directors 2026

Provides the financial modelling framework for quantifying the 84% cost savings and break-even calculations for open-source AI infrastructure migration discussed here.

Agentic AI 2026: The Complete Guide for UK Businesses

Explains the agentic AI systems whose geometric token consumption is the primary driver of the budget crises and cost routing strategies explored in this analysis.

RAG for UK Enterprise 2026: The Definitive Guide

Covers RAG pipeline implementation on sovereign UK infrastructure, eliminating the data sovereignty vulnerabilities of cloud-hosted knowledge base solutions covered in this article.

📚 Explore More Resources

Recommended Tools

ClickUp

"One app to replace them all. Yes, even that messy one."

$12/month

Free plan

Affiliate Disclosure

Close

"Built by sales people, for sales killers."

$49/month

14-day trial

Affiliate Disclosure

Ready to Transform Your Business with AI?

Discover the perfect AI agent for your UK business. Compare features, pricing, and real user reviews.